Shortages & Geopolitical Pressure: Almonty's Industrial Business Model Reimagined

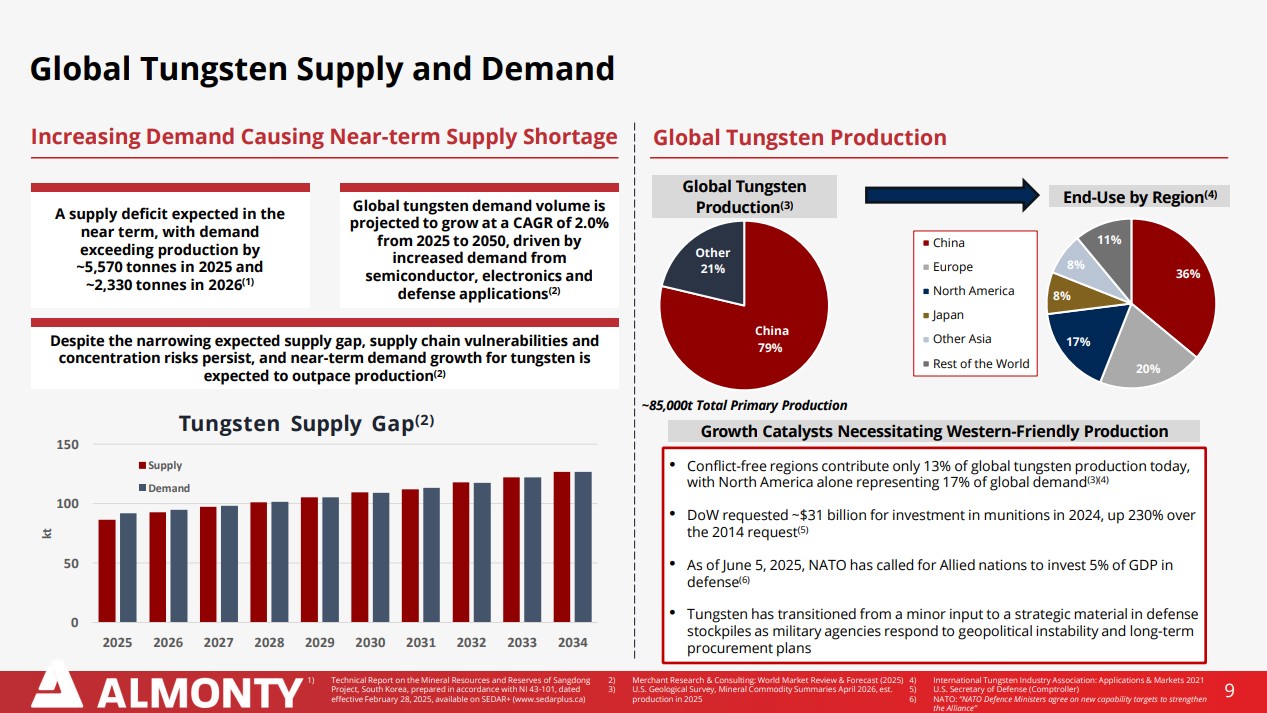

The Western world is facing a raw materials crisis with explosive geopolitical implications, as around 70% of the most important critical metals are still mined in China today. Now, China has drastically tightened its export controls on critical minerals. This primarily affects strategically important metals such as gallium, germanium, antimony, and, more recently, tungsten. These raw materials are indispensable for the defence industry, semiconductor production, and high-tech manufacturing. For many of these raw materials, China dominates the entire supply chain, from mining through processing to refining. For some metals (e.g., gallium and graphite), their global market share exceeds 80-90%. Countries such as the US, Germany, Japan, and South Korea are particularly affected, as they rely on these metals for semiconductors, batteries, chips, lasers, fibre-optics, wind turbines, and electric vehicles. Almonty Industries (WKN: A414Q8 | ISIN: CA0203987072 | Ticker Symbol (FRA/USA): ALI/ALM) is already positioned to fill the looming gap.

Almonty Industries is increasingly evolving from a traditional mining developer into a strategically positioned industrial supplier of critical metals. At the heart of the business model lies not only short-term raw material extraction but also the long-term securing of tungsten for Western customers. In a model that is almost akin to a partnership, CEO Lewis Black has been focusing for several months on integrated value chains that span from extraction and processing to reliable off-take agreements. This structure reduces dependence on volatile spot markets and shifts the focus to predictable cash flows. It is particularly relevant that Almonty operates specifically in markets where geopolitical factors increasingly dominate pricing. This creates a business model that is shaped more by strategic demand than by traditional commodity cycles, opening up correspondingly more stable prospects.

Sangdong: The Relaunch of a Key Global Mine

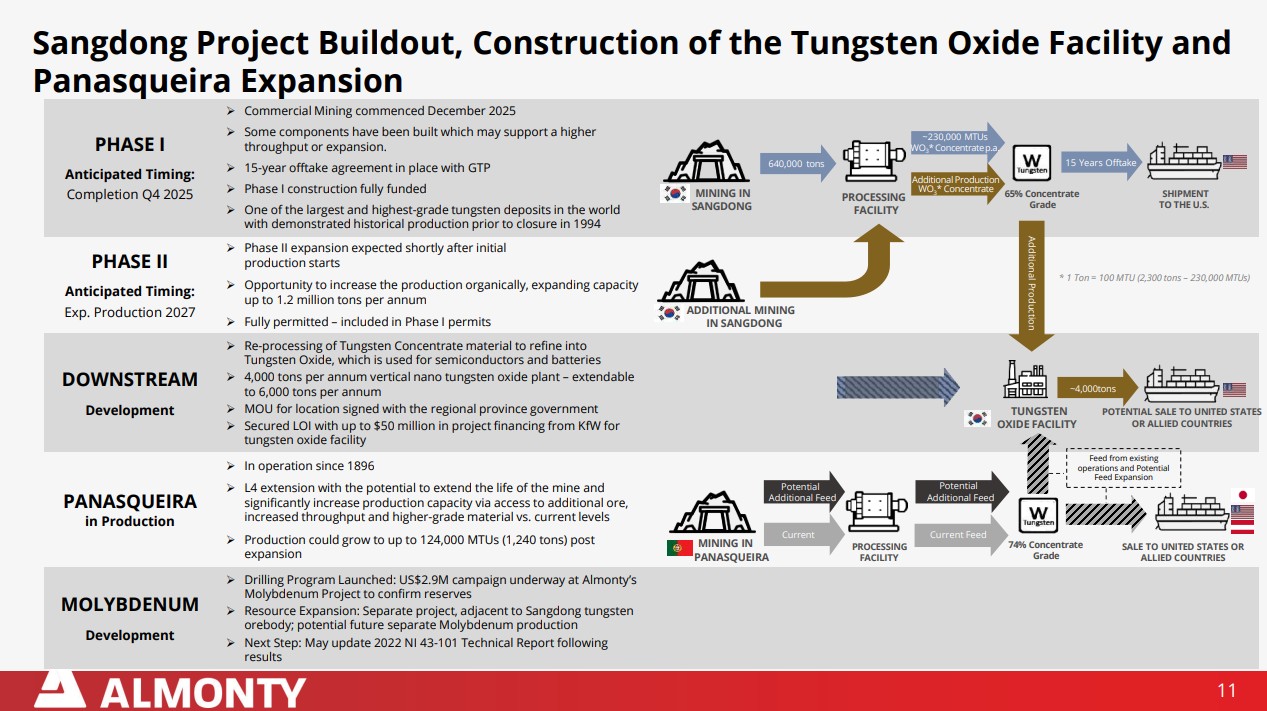

The successful commissioning of the Sangdong mine in South Korea marks a decisive turning point in the company's history. After decades of shutdown, one of the largest tungsten deposits outside China has been brought back into production. The geological conditions are considered exceptional, particularly due to the comparatively high ore grade, which significantly improves the economic efficiency of mining. As production ramps up, a new industrial base is emerging that can deliver stable output for decades to come. At the same time, the project is being expanded in phases to further increase capacity and realize economies of scale. As a result, Sangdong is increasingly becoming a central pillar of Western raw material supply and a potential game-changer in the global tungsten market.

"In the first half of 2026, a ramp-up to a throughput of 640,000 tons of tungsten ore annually is expected to be achieved."

A key factor in Almonty's success lies in the consistent securing of future production through long-term off-take agreements. These off-take structures create a direct link between production and end-user industrial demand while simultaneously reducing dependence on short-term price fluctuations. This is complemented by a significantly strengthened capital base, which gives the company leeway to ramp up projects without immediate financing pressure. Crucial to this is the combination of stable minimum prices and the opportunity to participate in rising market prices. This structure ensures a healthy balance between security and earnings potential.

Overview of Catalysts for the Near Future

- Phase 1: Commissioning and ramp-up at the Sangdong mine in South Korea are proceeding according to plan

- Phase 2: Increase in mill capacity or construction of a new facility to a target of 1.2 million MTU per year

- Tungsten: 15-year off-take agreement with GTP (USA) in place

- Increase in output at the Panasqueira mine in Portugal to up to 124,000 MTU through expansion

- Molybdenum drilling program launched

- Processing of tungsten concentrate into tungsten oxide, which is used for semiconductors and batteries

- LOI for downstream project financing of USD 50 million with KfW

- Low production costs estimated at USD 126.80 per MTU (APT) - Current market price > USD 3,000

- Production in the US: Reactivation of the historic mine in Montana

At the 19th International Investment Forum (IIF) today, May 20, CEO Lewis Black will, as always, offer deep insights into the world of tungsten mining. Click here to register for free.

Analysts Agree: Price Targets for Almonty are Based on the Tungsten Price

Although the range of expectations varies widely, the estimates all point in the same direction. Analysts anticipate massive jumps in revenue and profits in the coming years, driven by the fundamental rise in tungsten (APT). The price per metric ton (MTU) exceeded USD 3,000 in May.

Sphene Capital analyst Peter Thilo Hasler has updated his calculations and sees significant upside potential to CAD 37.40 (from CAD 20.10). The Munich-based expert expects significant revenue of CAD 218 million in 2026 and a corresponding EBIT of CAD 61.6 million, assuming operations commence by the end of 2025. Bottom line, a net profit of CAD 38 million, or CAD 0.13 per share, is projected to be achievable. For 2027, revenue figures jump to CAD 1.017 billion, pushing EBIT and net profit to CAD 629 million and CAD 493 million, respectively. In terms of earnings per share, this translates to CAD 1.75. At current prices around CAD 22.60, the stock would thus be valued at a 2027 P/E ratio of 12.9.

Texas Capital Securities also sees dynamic growth: USD 282 million in revenue in 2026, rising to USD 676 million the following year—and derives a price target of USD 25 (CAD 34.20) from this. Other firms calculated the following price targets: Couloir Capital CAD 19.30, Oppenheimer CAD 22.00, and GBC CAD 28.60. The variation in target prices fluctuates with expectations for the tungsten price. Despite currently high spot prices, some firms anticipate average prices in the range of USD 1,200 to 1,800 per MTU (APT) in the coming years. The stock's performance is therefore likely to be driven by the free cash flows achievable in each quarter, assuming stable and rising production volumes.

Conclusion: Reassessment of an Emerging Industry Player

The tungsten market is in a phase where geopolitical factors are increasingly overshadowing traditional market mechanisms. In this environment, Almonty is one of the few suppliers outside China that already possesses scalable production capacities. The combination of high-grade deposits, long-term off-take agreements, and growing strategic importance creates an exceptional starting position. At the same time, it is becoming clear that the structural scarcity of critical metals is not a short-term phenomenon but remains a long-term trend. For investors, this results in an asymmetric risk-reward profile that is heavily influenced by the operational execution of the ramp-up. The decisive variable thus remains the pace at which the market fully integrates this new industrial reality into its valuation.

Analysts' assessments increasingly reflect the company's structural transformation rather than its previous perception as a project developer. Some research firms particularly emphasize the combination of rising production and a structurally tight tungsten market. The forecasts for revenue and earnings thus point to a clear growth trajectory, though they differ in the pace of implementation. Crucially, the market is increasingly pricing in not only operational risks but also strategic relevance. This is gradually shifting the valuation logic toward an industrial multiple approach. Overall, the picture emerging is of a company in the midst of a revaluation that has not yet reached its endpoint.

Conclusion: Risk-aware investors can use the consolidation of the past few days to just under CAD 23.00 to strengthen their positions. Those who control or secure access to critical raw materials today are not only sitting on a source of industrial value creation but also on a geopolitical lever. In the long term, therefore, security premiums should be priced in alongside the pure production valuation. Analysts' price targets around CAD 30 reflect this and are quite plausible from a 12-month perspective, though likely significantly too low in geopolitical borderline scenarios.

Click here for the latest video featuring CEO Lewis Black with IIF host Lyndsay Malchuk.

This update follows our initial Report 12/2021.