Cost pressure increases, and sales prices do not follow suit

The continuing rise in energy and raw material prices is forcing battery manufacturer Varta to suspend its targets. The forecasts for sales and earnings for the current year and the third quarter, which have already been revised twice, can no longer be maintained. The currently high procurement prices for raw materials, especially energy, can only be passed on to customers to a limited extent and with a delay, as there are fixed supply contracts in the order business. They can only be changed in the medium term through new negotiations and the inclusion of additional clauses for the procurement side. In addition, two large orders from the important Microbatteries division have been delayed. The Varta share price plummeted by up to 39% to its lowest level since May 2019 following the news and reached lows of below EUR 32 over the rest of the week.**

this is how many cells Varta AG produces per year.

Investors have major concerns at the moment. On the one hand, high manufacturing costs in Europe bring out the fear of battery competition from overseas. This mainly concerns the existing business potential with Apple's latest generation AirPods Pro. Since things have not been going so well at Apple for a few weeks either, order placements are likely faltering here. After all, Europe is the most important sales market for the Californian tech group's products, alongside North America. On the other hand, Varta has been struggling with generally weak demand for some time now. However, there is interesting growth potential in the area of energy storage.

Because, among other things, many customers are missing important parts to produce wireless headphones - the once booming main business with lithium-ion button cells was already struggling at the start of the year. The outlook had already been revised at the beginning of August. However, most recently, Group CEO Herbert Schein had still considered annual sales of EUR 880 to 920 million and EBITDA of EUR 200 to 225 million possible. Both have now been discarded.

Ongoing supply chain issues and delayed projects

Like other high-tech sectors, Varta is struggling with ongoing supply chain issues and the ever-increasing cost of production factors. A big question mark looms, especially for the upcoming winter months, as gas is also an important factor in production. Pressure is, therefore, likely to remain high for the time being. Only when it becomes apparent at some point that the Group is also profitable again in the CoinPower segment and can land a market success with its investments in the lucrative e-mobility segment is the overall situation likely to change. The weak euro makes raw material purchases expensive on the one hand, but should support the internationally active Varta in exports. On the energy supply issue, the Company remains dependent but can absorb possible reductions.

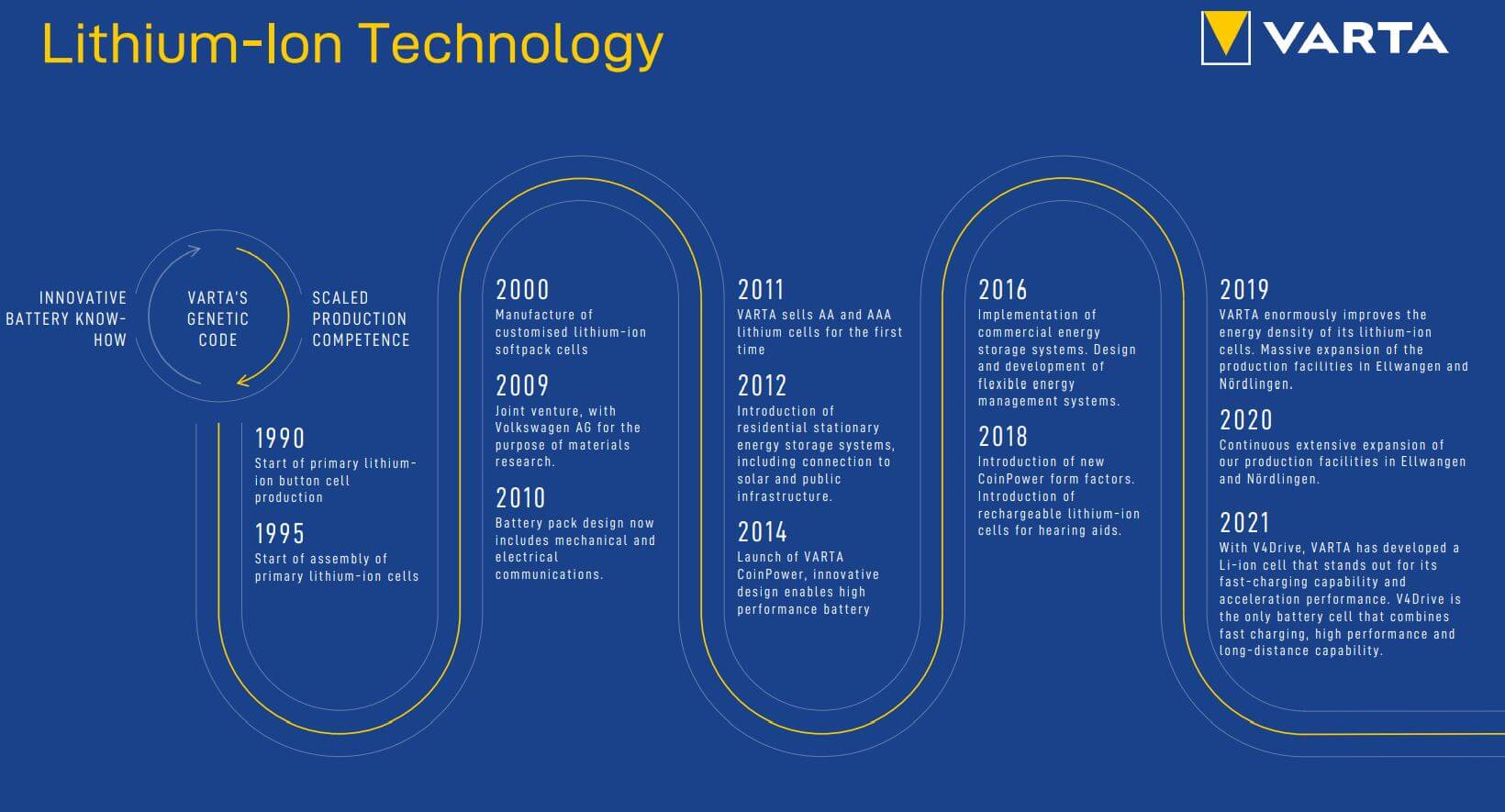

What is the status of electric mobility?

The market is still waiting for a super battery for electromobility. After several announcements at the beginning of the year on the subject of high-performance car batteries, the market still assumes that the medium-term plan for the e-offensive is in place. However, it will probably take more time than expected. In recent publications, management has emphasized that everyone in the industry is currently talking to everyone else. That means the first partnerships could sometimes come as a surprise to the market. **However, the first deliveries to OEM partners will take place in 2024; test production of 10,000 round cells per week is currently underway.

Freyr Battery from Norway holds good cards

The Norwegian competitor Freyr Battery is also making a name for itself. Everything is probably going according to plan here because, as with Varta, the first batteries are expected to roll off the production line in 2024. The share price is higher among analysts, and they are constantly outbidding each other with new price targets. This may be due to the fact that Freyr is less broadly positioned and obtains Norwegian energy; thus, the raw materials crisis does not affect the Company as much. Over the year, Freyr Battery has gained over 50% - there is no trace of gloom here.

There were nevertheless a few notes from the IIF

Varta AG presented itself on September 27 at the 4th International Investment Forum (IIF) in its usual manner of last PR appearances. IR boss Bernhard Wolf did not address the repeated profit warning until the Q&A session and did not have any slides on the specific situation. Understandable since the Board of Management has also suspended any forecast. With the mentioned delay with two larger customer orders, it was put into perspective that delays are expected, but the negotiated acceptances could become load-bearing nevertheless. Again, Wolf focused on the broad product range, which could again prove to be a solid risk mix in the future. 2022 is a difficult year of transition for Varta, but progress in the V4Drive area is tangible. As usual, the new cells should come from southern Germany, and Romania was also mentioned as a possible location. At Varta, the focus has been on its own development services and cooperation for years; the takeover of another provider is not on the agenda. Likewise, Wolf does not think a competitor will turn up at parent company Montana Tech to bid for Varta.

Analysts correct their forecasts

For Varta analysts, adjusting expectations with this frequency is not easy because, after all, the studies should also reflect the long-term business success of the Ellwangen-based company. Despite this, the latest consensus estimates for 2022 earnings per share of EUR 0.48 to EUR 1.67 are trending down from a high of EUR 2.72 at the beginning of the year. The coming years are also subject to a correction of between 20% and 30%. The downward revision for 2022 is already more than 40% on average. However, the share price is already underwater by 72% on a 12-month view. It shows that there was probably a positive bias in rising markets, which has not yet been reduced accordingly. Nevertheless, the analysts are not entirely negative. While Berenberg (target lowered from EUR 75 to EUR 45) and DZ Bank (target lowered from EUR 69 to EUR 40) rate the stock as Neutral and Hold, Warburg now sees a Buy after their longer "Sell" rating despite lowering the price target from EUR 65.20 to EUR 53. Realism is now coming to light in the strong corrections, especially since the bank also reduced the sales estimates. Overall, the revisions are likely to continue for some time.

The usefulness of stop prices

Since the turn of the year, the share has lost almost two-thirds of its valuation. Compared with the record high of just over EUR 180 in January 2021, the share has now lost over 80%. Market capitalization has fallen to EUR 1.44 billion, which once stood at over EUR 7 billion. In parallel, the market has to come to terms with an almost 40% drop in profits. After this sell-off, the share will have to convince investors with solid fundamental data in order to lure them back out of the woodwork. Progress in electromobility could help. With its V4Drive development program, the Company is currently supplying over 10,000 cells per week for testing purposes to a major OEM that has not yet been named.

With the current business plan, the share is now only valued at a price-to-sales ratio of 1.8; this ratio has reached values of over 4 in the past. Even in the current environment, it is expected that Varta will be able to sell its output, but the achievable profit will be eaten up to a large extent by the high costs. Here, the consensus values could still lag far behind reality due to the delayed adjustment because it must still be feared that the second half of the year will also run without significant improvements. The Q3 figures on November 5, 2022, could provide more precise insight. This will be really exciting.

Interim conclusion

After the renewed profit warning, the share price halved in September from EUR 65 to EUR 32. The fluctuations are enormous, and in the course of the day, +/-10% is no longer a rarity. Of course, there is strong selling pressure on other technology stocks as well, but in the case of Varta, the burdening fundamental data are on top of that. An indication of the drama is illustrated by the consensus value for the price target. According to surveys by S&P Market Intelligence, it has fallen from EUR 99.8 to EUR 56.2 in just 3 months. However, there will likely be further revisions. Technically, the share price would have to climb back up to the EUR 60 mark and later to the EUR 85 mark, which is probably not expected from today's perspective. In the long-term chart, the correction could even approach the zone around EUR 25. Investors should keep their watch position until the fundamental scenario for commodity-heavy producers develops for the better in Germany or Varta can show new successes in some key sectors.

The update is based on our initial Report 11/21