The Market No Longer Values Resources Alone: It Values Security of Supply

The market is starting to take notice! The tungsten market has undergone a fundamental shift within just a few quarters. While investors used to focus primarily on deposit size, ore grades, or production costs, a different factor has now taken center stage: the secure supply to Western industries of a raw material that has become indispensable for defense, aerospace, semiconductors, and modern high-performance technologies. Tighter export restrictions from China, rising defense spending by NATO countries, and the increasing decoupling of global supply chains are changing the valuation criteria for the entire industry. As a result, companies with secure production outside China are no longer viewed exclusively as traditional mining companies but increasingly as strategic building blocks of Western industrial policy. In this environment, Almonty Industries (WKN: A414Q8 | ISIN: CA0203987072 | Ticker Symbol (FRA/USA): ALI/ALM) continues to evolve steadily and, within just a few weeks, has achieved several milestones that mark the transition into a new phase for the company.

Sangdong Crosses the Critical Threshold into Industrial Production

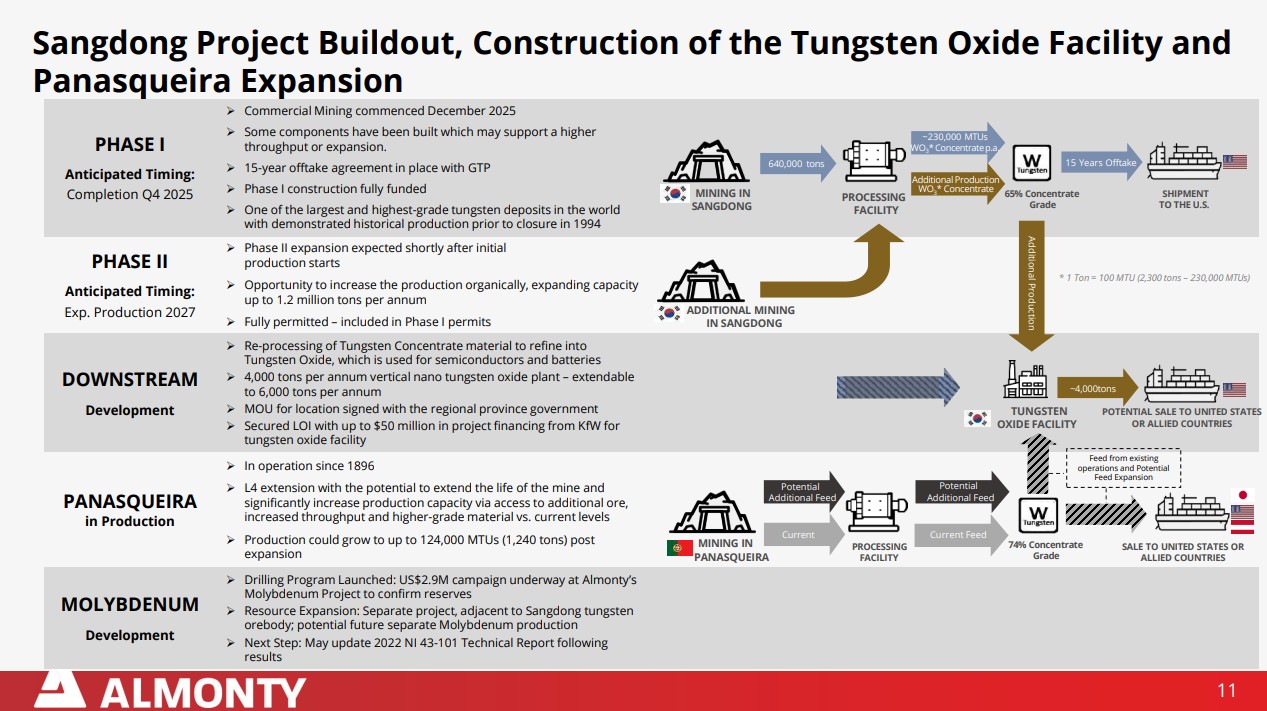

With the start-up of the processing plant in Sangdong in early July, a step was taken that means much more to Almonty than just another project announcement. For the first time, mined ore is being continuously processed into marketable tungsten concentrate, transforming a long-standing development project into an operational production site. For the start-up, the company is drawing on an existing ore stockpile of nearly 140,000 metric tons, allowing the plant to ramp up in a controlled manner while ensuring sufficient material is available for several months of processing. It is particularly noteworthy that even the material currently being used has ore grades significantly higher than those of other existing tungsten mines, thereby improving the economic margin already in the start-up phase. As production stability increases, higher-grade areas of the deposit are to be developed in the future, which could further increase both metal yield and profitability.

However, the significance of this production launch extends far beyond operational progress. In a market characterized by a structural supply shortage, what counts today is not so much the theoretical resource as the ability to deliver physical material on short notice. It is precisely this delivery capability that is increasingly becoming the most important competitive advantage for Western producers. While many projects worldwide still require years to obtain approval or financing, Almonty is already beginning to supply the market with additional material. This also shifts the perception of the company from a "future story" to that of an actual producer with immediate cash flow potential. A key factor in Almonty's success is its consistent ability to secure future production through long-term offtake agreements. These offtake structures create a direct link between production and end-user industrial demand while simultaneously reducing dependence on short-term price fluctuations. Key to this is the combination of stable minimum prices and the opportunity to participate in rising market prices. This structure ensures a healthy balance between security and earnings potential.**

Montana Takes Center Stage: The US Reserve as a Long-Term Growth Step

In addition to South Korea, the US project pipeline is also gaining increasing importance. The Gentung Tungsten Project in Montana could represent another pillar of Western supply in the long term and holds particular strategic significance, especially against the backdrop of US resource policy. The latest exploration results from the immediate vicinity underscore the region's geological potential. At the Pioneer Tungsten Project, numerous samples with significantly elevated tungsten values were identified, including peak values of over 3,000 ppm WO₃. It is highly significant that the mineralization exhibits characteristics comparable to those of the nearby Gentung structures, thereby confirming the importance of the entire district for future tungsten production.

Montana has historically been linked to strategic tungsten mining in the US. Earlier production phases in the 1950s and 1970s show that the region was already used as an important source of supply during commodity shortages. Today, this location is taking on new significance due to the growing demand for non-Chinese supply chains. For Almonty, Gentung could thus represent a strategic complement to Sangdong in the long term and further strengthen its position as a Western supplier. The combination of South Korean production, a Portuguese base, and an American project pipeline creates a diversified production network that is increasingly valuable in its own right within the critical raw materials sector.

Molybdenum as an Additional Value Driver: Sangdong Is Evolving into a Strategic Raw Materials Platform

However, Almonty's growth prospects are not limited exclusively to tungsten. In parallel with the production ramp-up, the company is investigating the adjacent molybdenum deposit at Sangdong and could, in the long term, develop a second strategic raw material source within the same infrastructure. The ongoing drilling program comprises a total of 26 drill holes with a total length of approximately 12,000 m. It is intended to confirm the historical mineralization and lay the foundation for a future resource definition. The results so far are encouraging, as the initial drilling data show grades comparable to those from earlier surveys, thereby supporting the geological continuity of the deposit. Should the size of the ore body be confirmed, Almonty could ramp up production without having to develop entirely new infrastructure.

Strategically, molybdenum is becoming increasingly important, as the metal is used in high-strength specialty steels for defense, aviation, power plants, and industrial applications. Demand is also rising due to new technological fields such as semiconductor production and modern energy systems. The combination with the existing Sangdong site is particularly interesting, as Almonty could leverage its mining expertise, processing capacity, and logistics infrastructure in multiple ways. This creates a potential scale effect that goes beyond a pure tungsten project.

An Overview of Near-Term Catalysts

- Phase 1: Commissioning and ramp-up at the Sangdong mine in South Korea are proceeding according to plan

- Phase 2: Increasing mill capacity or constructing a new facility to a target of 1.2 million MTU per year

- Tungsten: 15-year offtake agreement signed with GTP (US)

- Increase in output from the Panasqueira mine in Portugal to up to 124,000 MTU through expansion

- Molybdenum drilling program launched

- Further processing of tungsten concentrate into tungsten oxide for semiconductors and batteries

- LOI for downstream project funding of USD 50 million with KfW

- Low production costs estimated at USD 126.80 per MTU (APT) vs. current market price > USD 3,000

- US Expansion: Reactivation of the historic mine in Montana

- Inclusion of molybdenum as an additional source of cash flow in South Korea

Institutional Investors Boost Confidence in the Growth Strategy

In parallel with operational progress, Almonty achieved one of the most significant financing milestones in its corporate history in June. The placement of a USD 700 million convertible senior notes offering met with such high demand from institutional investors that the full over-allotment option was also exercised. After deducting issuance costs, the company received approximately USD 773 million, thereby securing an exceptionally strong balance sheet for the upcoming development phases. This capital raise not only finances individual projects but also significantly increases the company's strategic flexibility. In an environment where critical raw materials are gaining geopolitical importance, financial strength provides a decisive advantage, as investments can be made independently of short-term capital market cycles. Above all, institutional investors signaled through their oversubscription that they no longer classify Almonty as a traditional small-cap explorer, but rather as a potential core supplier for Western tungsten supply. This development is also likely to change perceptions in the capital markets going forward. As a result, the valuation logic is increasingly shifting away from speculative resource models toward the industrial multiples of successful producers.

Analysts Do the Math: Tungsten Price Sets the Pace for Valuation Jumps

Analysts' estimates diverge in the details but converge on the overall trend: the tungsten price serves as the central valuation anchor for Almonty. With prices recently exceeding USD 3,000 per MTU, significant earnings leverage is coming into focus. Sphene Capital anticipates a steep ramp-up following the start of production in late 2025. Revenue of approximately CAD 218 million and net income of CAD 38 million are expected for 2026, with revenue over CAD 1 billion and earnings per share of CAD 1.75 in 2027. This currently results in a moderate forward P/E ratio in the low teens—while offering significant re-rating potential. Texas Capital also anticipates dynamic scaling and derives a price target equivalent to over CAD 34. A recent update from Cantor Fitzgerald, dated July 1, sets a price target of CAD 36.10—about 50% above the current level. Other valuations fall within a wide range, depending on the assumed tungsten price. So everything revolves around the tungsten price: it is the direct driver of the billions in cash flows achievable in the medium term. The market is pricing in various cycles, typically ranging from USD 1,200 to 1,800 per MTU. Ultimately, however, operational performance remains decisive. As production increases, the valuation is likely to be increasingly guided by realized free cash flows and margin levers.

Conclusion: Almonty Is Evolving from a Commodity Play into a Strategic Industrial Company

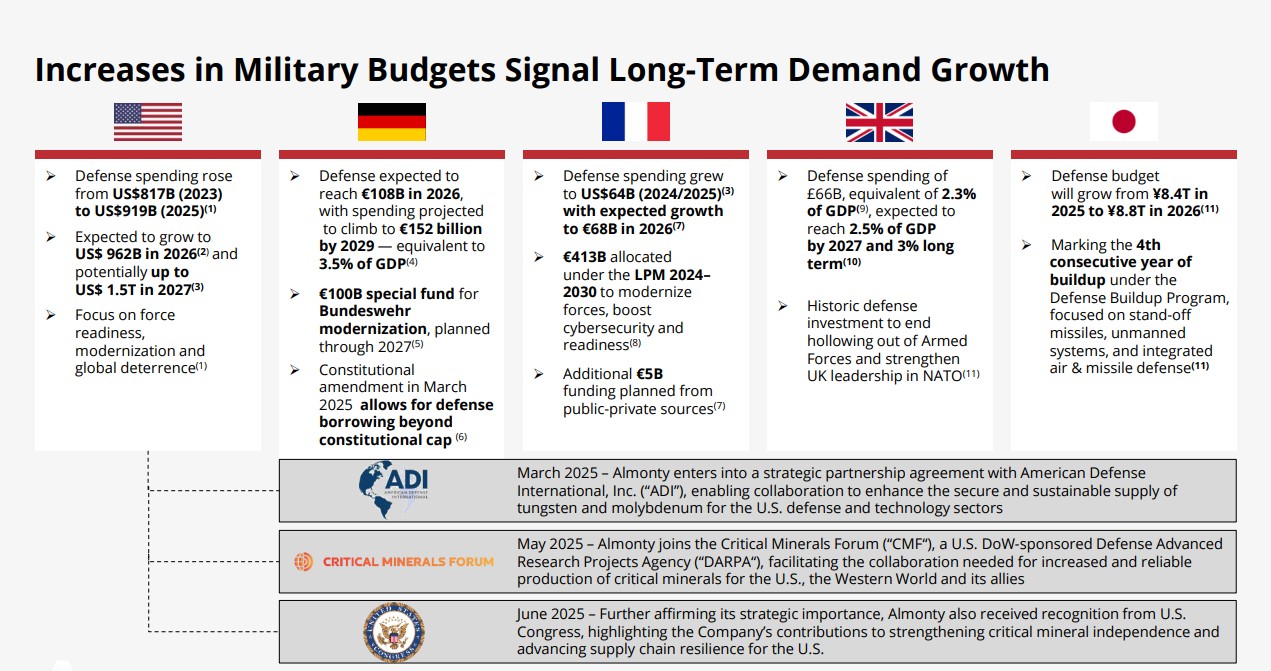

The past few months have marked a fundamental shift for Almonty Industries. With the start of production in Sangdong, the successful large-scale financing round, and its inclusion in major US indices, the company has cleared several critical hurdles at once. The investment story is thus no longer based exclusively on future resources, but increasingly on actual production, strategic demand, and growing institutional attention. Nevertheless, the tungsten market remains the key driver, as the combination of limited supply, geopolitical uncertainty, and rising demand from the defense and high-tech sectors creates a structurally supportive environment. Planned NATO defence spending indicates that investment is set to roughly double from levels seen five years ago.

Of course, operational execution remains the most important valuation factor. The successful ramp-up of the Sangdong mine, potential expansions through Phase II, and the development of additional projects will determine how effectively Almonty can convert its strategic position into actual earnings. The company's recent capital measures provide it with considerable financial flexibility for this purpose and reduce short-term growth risks. In summary, investors are investing in a company that is benefiting immensely from the geopolitical shift in critical metals and, at the same time, is just beginning to fully leverage its industrial platform commercially.

Risk-tolerant investors should use the recent sideways phase below CAD 21.00 as a tactical entry opportunity. After all, those who secure access to critical raw materials today are not only positioning themselves along the industrial value chain but are also benefiting from strategic scarcity premiums in the geopolitical context. In addition to traditional valuation metrics, security-driven premiums are thus increasingly coming into focus. The projected price targets around CAD 30 reflect this scenario and appear well within reach over a 12-month horizon—though they are on the conservative side given the heightened geopolitical conditions.

Click here for the latest video featuring CEO Lewis Black and IIF host Lyndsay Malchuk.

This update follows our initial Report 12/2021.