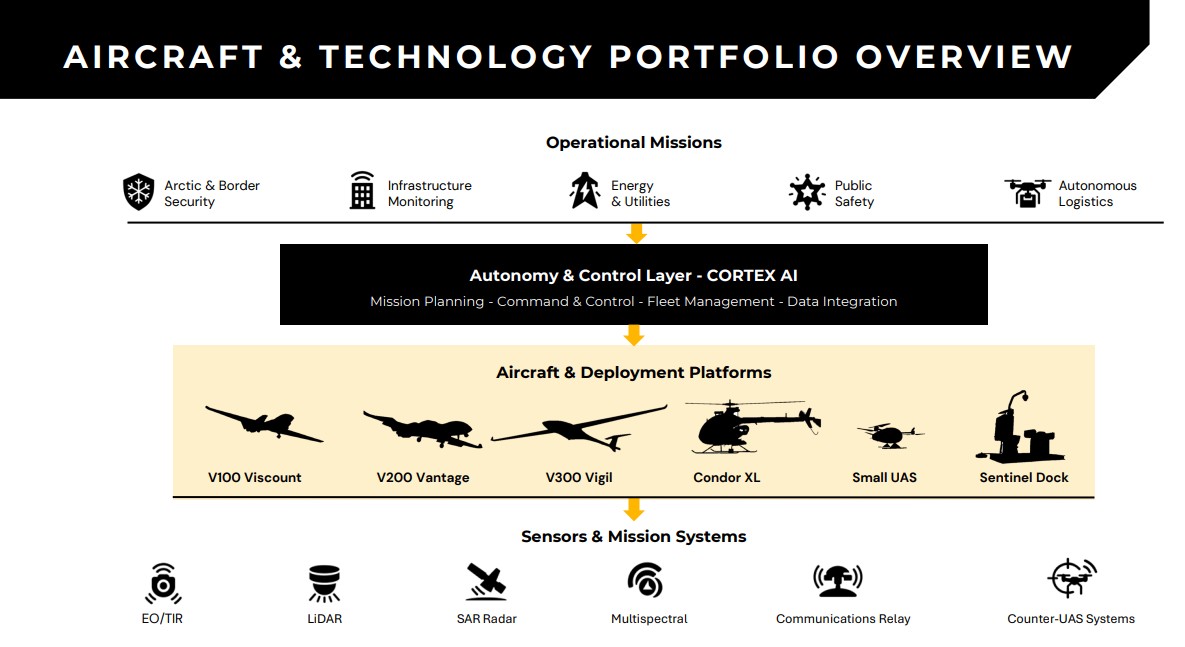

From Flight Service Provider to Architecture for Autonomous Air Systems

Volatus Aerospace Inc. (TSX-V: FLT | WKN: A2JEQU | ISIN: CA92865M1023) is clearly moving away from the traditional drone service business toward becoming an integrated technology and systems provider for autonomous air operations. The focus is no longer on individual aircraft but on mapping out complete mission chains encompassing data acquisition, processing, control, and analysis. This shift is fundamentally changing the company's business model: away from project-based operations and toward recurring, software- and service-driven revenue streams. The course has been set, the coffers are full—now it is time to go all out!

The New War Economy: Drones as the Pacesetters of Modern Conflicts

The current shift in military practice acts as an external accelerator for the entire unmanned systems sector. Conflicts in Europe have shown that logistics, reconnaissance, and precision are increasingly driven by drone swarms and AI-powered analysis systems. Traditional assumptions about camouflage and target concealment are losing their effectiveness because object recognition today relies primarily on pattern analysis, depth structure, and thermal signatures.

This is creating a new balance between offence and defence. Every new class of drone immediately generates demand for countermeasures, sensor fusion, and electronic detection. As a result, the market is not developing linearly, but systemically—as a perpetual arms race between autonomous platforms and anti-drone technologies. This feedback loop drives structural growth for well-positioned, vertically integrated providers. Companies like Volatus that actively pursue both trends can position themselves at the intersection of these trends with their service portfolio. Public-sector and even military providers are seeking this active networking.

High-Level Validation Provides a Solid Foundation for Investment

The US Department of Defense provides Volatus with strong external validation through its Phase II qualification in the "Drone Dominance Program" (DDP). The multi-billion-dollar program relies on live-fly tests under realistic interference and operational conditions and could lead to prototype and production orders in the triple-digit millions in the next phases. For Volatus, a successful run through the program could mark a turning point, as supply chains close to NATO are gaining significant strategic importance in this geopolitically tense environment.

The DDP is a mega-project with a budget of over USD 1.1 billion. Winners of the regular test phases (known as "Gauntlets") can look forward to follow-on orders worth millions and long-term procurement contracts. While approximately 30,000 drones were ordered in Phase I (early 2026), order volumes will rapidly double or triple in subsequent phases. Starting in Phase II (mid-2026), the use of engines, batteries, or critical electronics from certain countries (particularly China) will result in immediate disqualification. The criteria are strict, but Volatus Aerospace is well-positioned to meet the requirements.

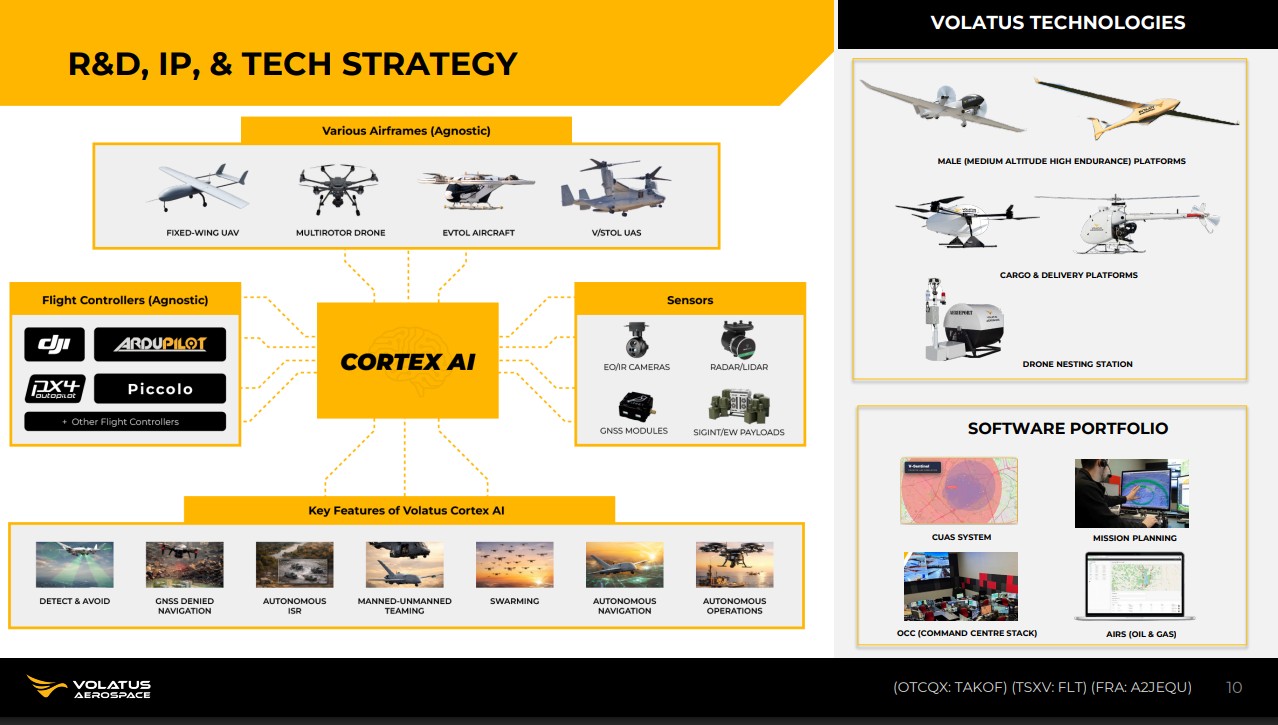

V-Cortex and SKYDRA: The Technological Backbone for Software and AI Monetization

The key driver of margins is increasingly found in the software and autonomy sectors. With the launch of V-Cortex, Volatus has introduced an AI-powered autonomy architecture developed entirely in Canada, which combines GNSS-independent navigation, edge computing, and mission-based decision-making logic. The platform is deliberately designed to be modular and is intended to integrate into air, ground, and maritime systems. Behind SKYDRA lies the rapidly growing market for counter-UAS solutions—that is, the detection and defence against hostile drones. Experience from current conflicts shows that protection systems against drone attacks are becoming a critical infrastructure standard. This is giving rise to a highly scalable software segment with potentially significantly higher margins than the traditional hardware business. The transition to recurring, data-driven revenue models could structurally alter the company's valuation profile and sequentially boost its revenue pipeline. The coming months will reveal where this journey is headed.

In the Battlefield: Technological Acceleration Through Real Combat Deployment

A strategic differentiator arises from systematic integration with Ukrainian innovation and defence networks. Through the UCan Brave Tech Center, Volatus gains access to technologies that originate directly from real-world operational environments and have been iteratively refined under extreme conditions. This form of "battle-tested innovation" shortens development cycles and significantly increases the practical relevance of new systems. Those who face the "enemy" and endure real-world stress tests identify requirement profiles and critical adjustment parameters.

At the same time, an industrial base for the integration and scaling of these technologies is being established in Canada, particularly in Mirabel. This is not merely a production site, but a system hub for development, assembly, training, and operational support. The combination of battle-tested software logic and Western industrialization creates a rare acceleration structure in the defence tech sector.

Financing, Contracts, and Government Demand as Catalysts

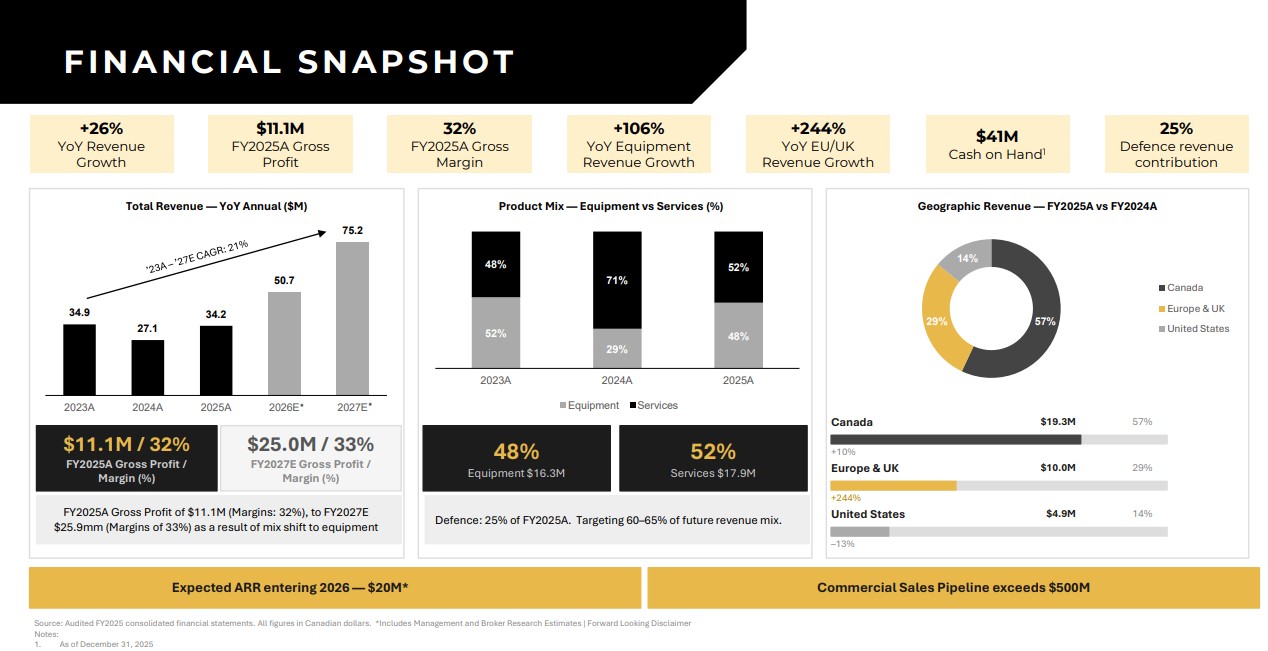

The latest capital measures underscore this phase of accelerated expansion. A bought-deal financing round—which was oversubscribed several times over and totaled more than CAD 30 million—significantly strengthened the balance sheet and expanded the investment base for production expansion and technology development. The funds are intended not only to strengthen the balance sheet but, above all, to scale industrial capacities. They are being directed specifically toward production expansion, platform development, and the establishment of recurring service infrastructures. This lays the groundwork for the company to structurally serve larger government programs and long-term defence contracts.

At the same time, the importance of training and education programs is increasing significantly, particularly within the NATO context. These programs are less cyclical than traditional hardware sales and generate stable, recurring revenue. As a result, the revenue base is gradually shifting toward predictable, long-term contract structures. A comparison of the most recently published figures for fiscal year 2025 with the outlook for fiscal years 2026/27 offers guidance on what investors can expect. Since the actual production rate in the context of geopolitical unrest is unknown, this outlook is also only an estimate**.

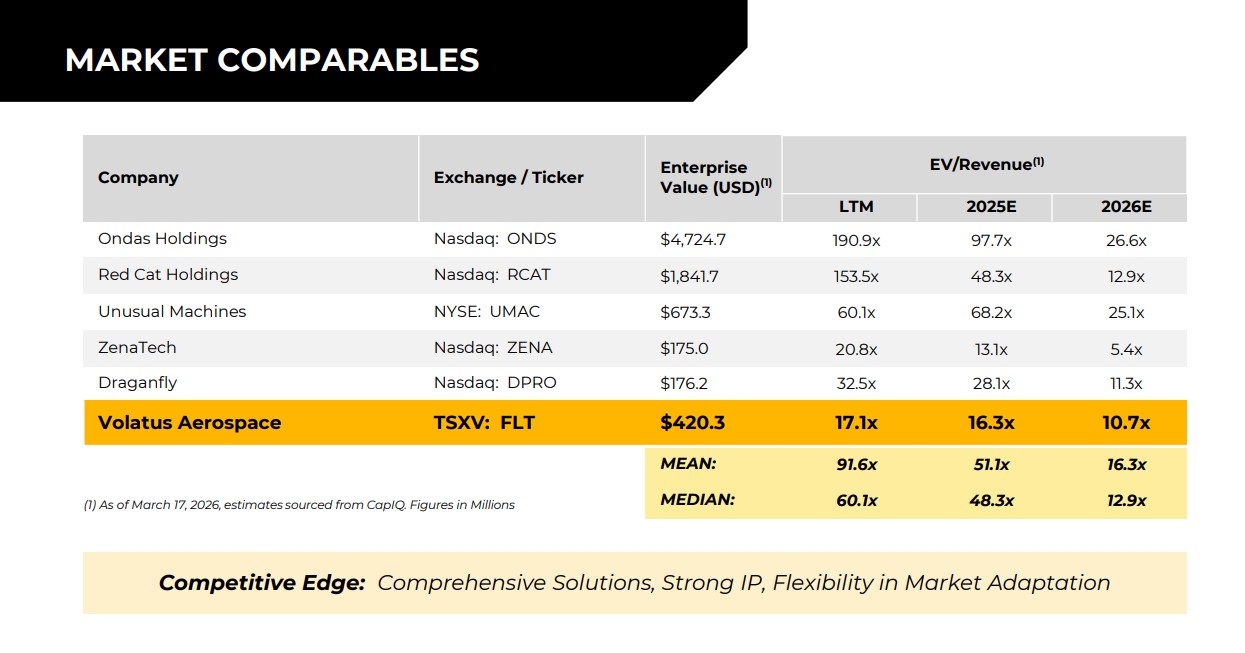

Valuation Discrepancy Between Growth Momentum and Market Capitalization

Despite rising operational activity, the valuation remains moderate compared to peers. Some competitors in the defence and drone segments trade at significantly higher revenue multiples, even though they exhibit similar or lower levels of diversification. Volatus, on the other hand, combines hardware, software, training, and services into an integrated model—an approach that competitors can only partially replicate.

The discrepancy between operational performance and market valuation opens up a potential re-rating scenario, provided that scaling in software and defence programs continues to gain momentum. The ability to systematically expand recurring revenue from SKYDRA and V-Cortex will be particularly crucial. In a market environment increasingly shaped by geopolitical demand and structural rearmament, this combination of platform depth and government demand could become a key valuation driver.

Investment Highlights

Volatus Aerospace (WKN: A2JEQU | ISIN: CA92865M1023 | Ticker Symbol: FLT)

- Highly specialized aerial data analysis as a unique selling proposition

- Evolving into a technical testing authority for critical infrastructure

- High security requirements from public sector clients ensure a steady deal flow

- International rearmament trends create strategic demand for defence solutions

- Limited competition due to mandatory certifications and training requirements

- Significant growth potential through international expansion in the medium term

- Scaling enables exponential growth for international expansion

- The use of Cortex AI and SKYDRA propels Volatus forward in major strides

- Integration into the North American defence ecosystem secures US and NATO contracts

- Highly liquid stock and a still-low market valuation of around CAD 435 million

Conclusion: A Company in Transition Toward Systemic Importance

Over the past few years, Volatus Aerospace has consistently evolved from a traditional provider of drone operations into a broadly diversified aerospace and defence tech platform. Today, the Canadian company integrates autonomous flight systems, AI-based control software, training programs, data analysis, manufacturing, and security applications. It is precisely this vertical integration that is likely to represent a decisive competitive advantage in a market environment increasingly shaped by technological sovereignty, resilient supply chains, and security-related applications. Additional momentum comes from close collaboration with NATO-affiliated institutions, a growing presence in the defence sector, and the company's role as a bridge between Canadian industrial capacity and innovations from Ukraine developed under real-world operational conditions.

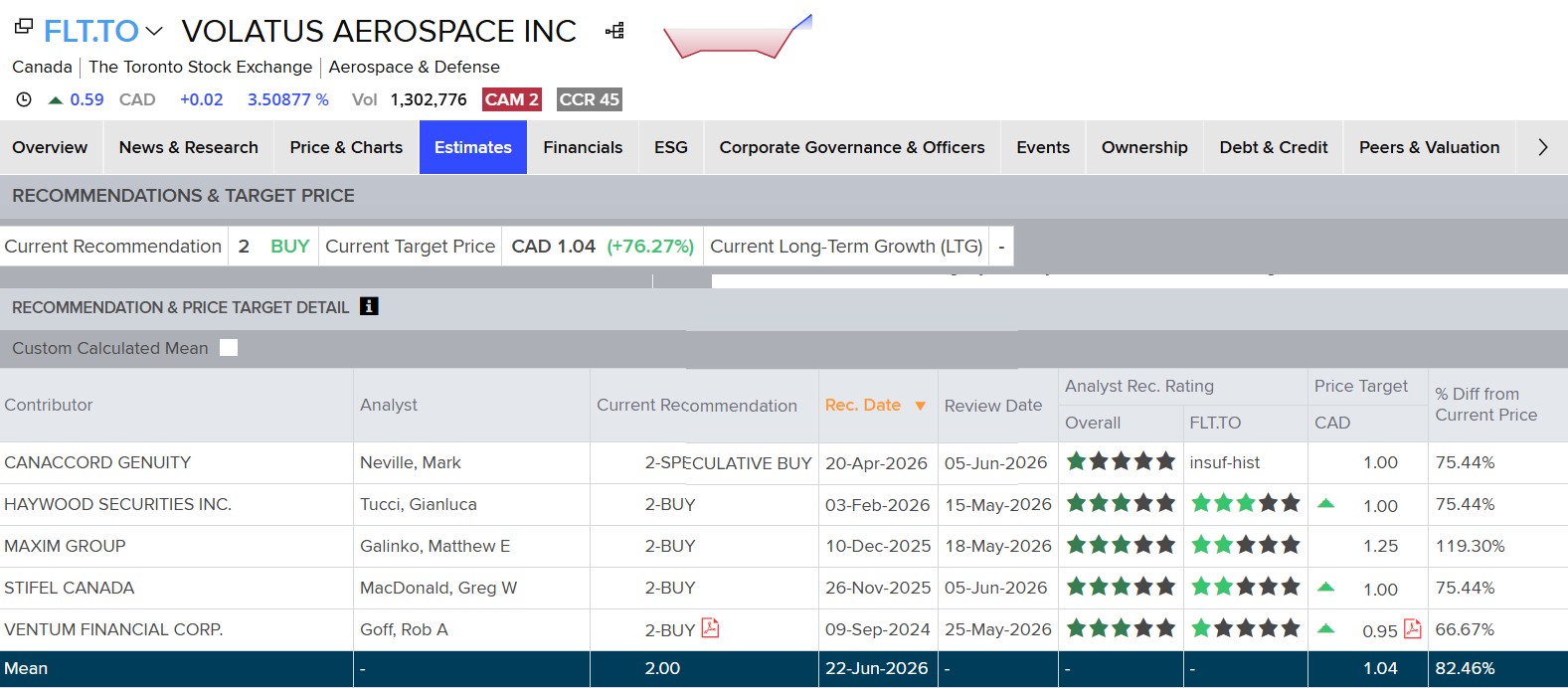

For investors, the question now comes to the forefront: when will the operational momentum be fully reflected in the valuation? With a significantly strengthened balance sheet, fresh growth capital, a project pipeline worth several hundred million dollars, and new technology platforms such as V-Cortex and SKYDRA, the groundwork has been laid for the company's next phase. While the market value still appears comparatively moderate, analysts already foresee significantly higher valuation levels of over CAD 1.00 over the next twelve months. The coming quarters will be decisive. If the company succeeds in converting the rising order intake into scalable revenue, higher margins, and sustainable profitability, the market's perception of the company could change fundamentally.

For dynamic investors, this presents a rare opportunity: a technologically well-positioned growth stock whose operational performance may still be one step ahead of the capital markets. A closer analysis of the trend over the past few quarters reveals that the operational foundation is growing at a rate similar to that of the overall order backlog. In other words, Volatus Aerospace has now streamlined its internal processes to the point where it can rapidly accelerate its growth trajectory. Looking ahead to the next 2 to 3 quarters, with increased visibility, there is clearly much more potential! Risk-aware investors with a medium-term horizon should therefore not miss the opportunity to buy in at CAD 0.60.

CFO Abhinav Singhvi explained the company's strategy and its 500 million dollar pipeline at the recent 19th International Investment Forum.

This update follows our initial report from March 2026. Click here for the initial report.