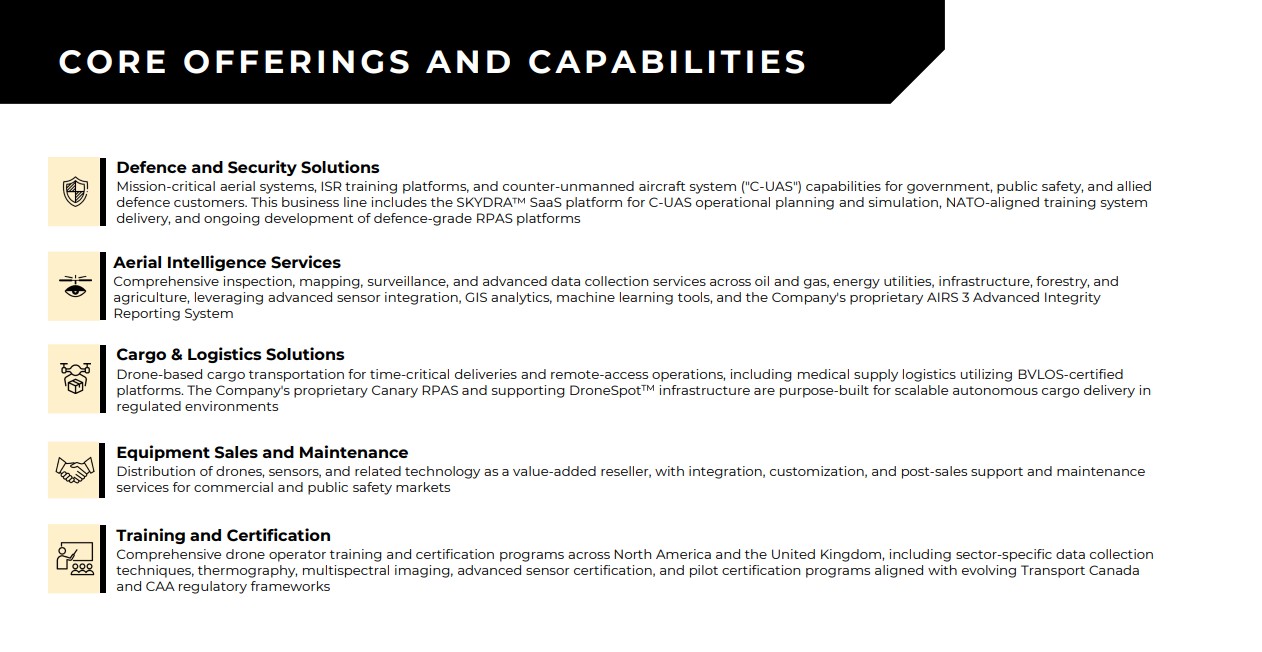

From Drone Provider to Integrated Autonomy and Defence Platform

Volatus Aerospace Inc. (TSX-V: FLT | WKN: A2JEQU | ISIN: CA92865M1023) is evolving from an operational drone service provider into a vertically integrated platform for unmanned aviation, AI-powered autonomy, and mission-critical data infrastructure. The business model is clearly shifting from project-based one-time revenues toward recurring service, training, and software revenues. The key is the integration of hardware, mission software, data analysis, and training within a closed ecosystem. In this way, Volatus addresses both civil infrastructure markets and the rapidly growing defence sector.

Confirmation From the Highest Level: Drone Warfare as a Structural Accelerator of Demand

The global security situation now acts as a permanent catalyst for demand for autonomous systems. The conflict in Ukraine demonstrates a new dimension of warfare: the mass deployment of drones to destroy logistics, infrastructure, and supply chains over long distances. At the same time, increasingly powerful countermeasures are emerging, such as AI-supported target recognition systems, which render even simple camouflage strategies like "zebra patterns" technically obsolete. Modern CNN-based classification models reliably recognize vehicle structures regardless of superficial visual distortions. A new structural factor is the transition to highly scalable, cost-efficient drone systems in everyday military operations. Systems in the low five-figure cost range are increasingly replacing traditional, significantly more expensive weapon platforms. This shift increases the demand for platforms that not only supply drones but also provide complete operational, analytical, and defence architectures. With a remarkable system logic, Volatus is positioning itself with its integrated approach combining training, operations, and software. And this trend is becoming increasingly pronounced!

The US Department of Defence provides Volatus with strong external validation through Phase II qualification in the "Drone Dominance Program." The multi-billion-dollar program relies on live-fly tests under realistic interference and operational conditions. It could open up prototype and production orders in the hundreds of millions in the next phases. For Volatus, a successful run-through could be a potential turning point, as NATO-aligned supply chains are gaining significant strategic importance in the current geopolitically tense environment.

V-Cortex and SKYDRA: Transition to Software and AI Monetization

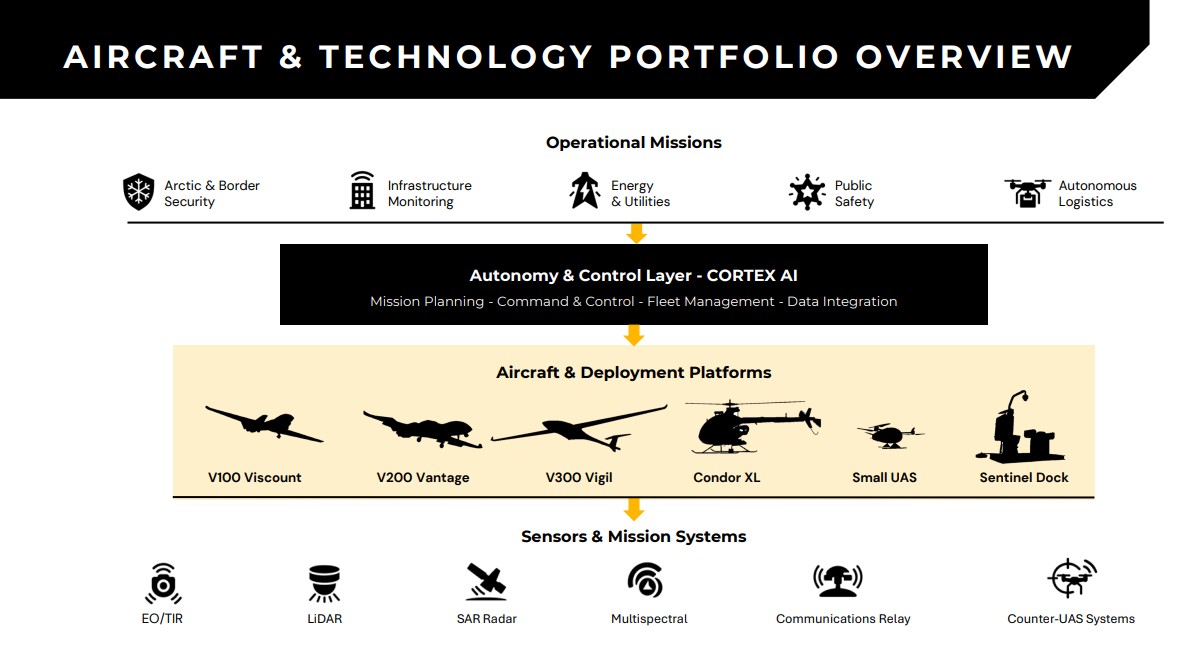

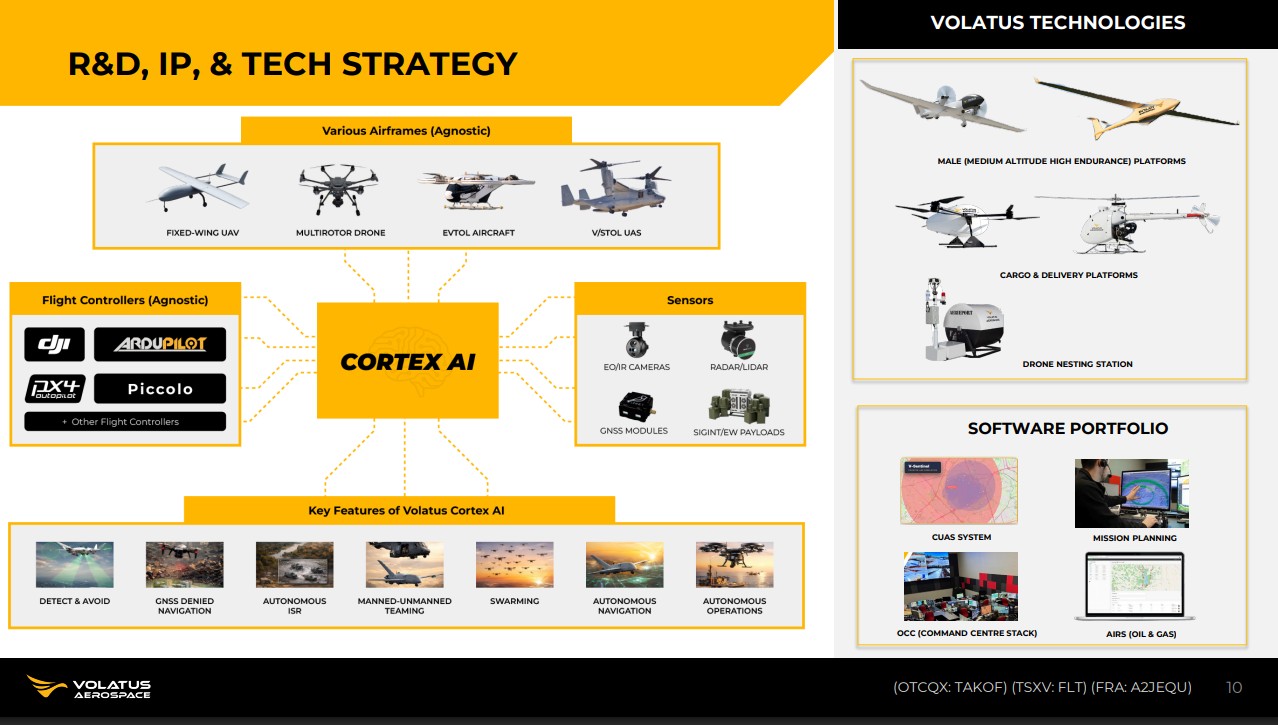

The key margin driver is increasingly in the software and autonomy sectors. With the launch of V-Cortex, Volatus has introduced an AI-powered autonomy architecture developed entirely in Canada that combines GNSS-independent navigation, edge computing, and mission-based decision logic. The platform is deliberately modular in design and is intended to integrate into air, ground, and maritime systems. Behind SKYDRA lies the rapidly growing market for counter-UAS solutions, i.e., the detection and defence against hostile drones. Experience from current conflicts in particular shows that protection systems against drone attacks are becoming a critical infrastructure standard. This creates a highly scalable software segment with potentially significantly higher margins than the traditional hardware business. The transition to recurring, data-driven revenue models could structurally alter the company's valuation profile and sequentially boost the revenue pipeline.

Canada-Ukraine Partnership as Operational Technology Transfer

A highly relevant strategic growth driver is the increasing integration with Ukrainian defence technology. Through the Memorandum of Understanding with the UCan Brave Tech Centre, Volatus gains access to battle-tested systems and tactical development experience from a real high-intensity conflict. The goal is to scale and industrialize these technologies for NATO and Allied markets. The new cooperation combines Ukrainian frontline experience with Canadian manufacturing and commercialization infrastructure.

Of particular relevance is the role of the Mirabel, Québec site, which is being gradually expanded into a production and integration hub for unmanned systems. This combination of field validation and industrial scaling creates a rare, strategically valuable development path in the defence tech sector.

Capital Influx, Industrial Scaling, and Order Pipeline

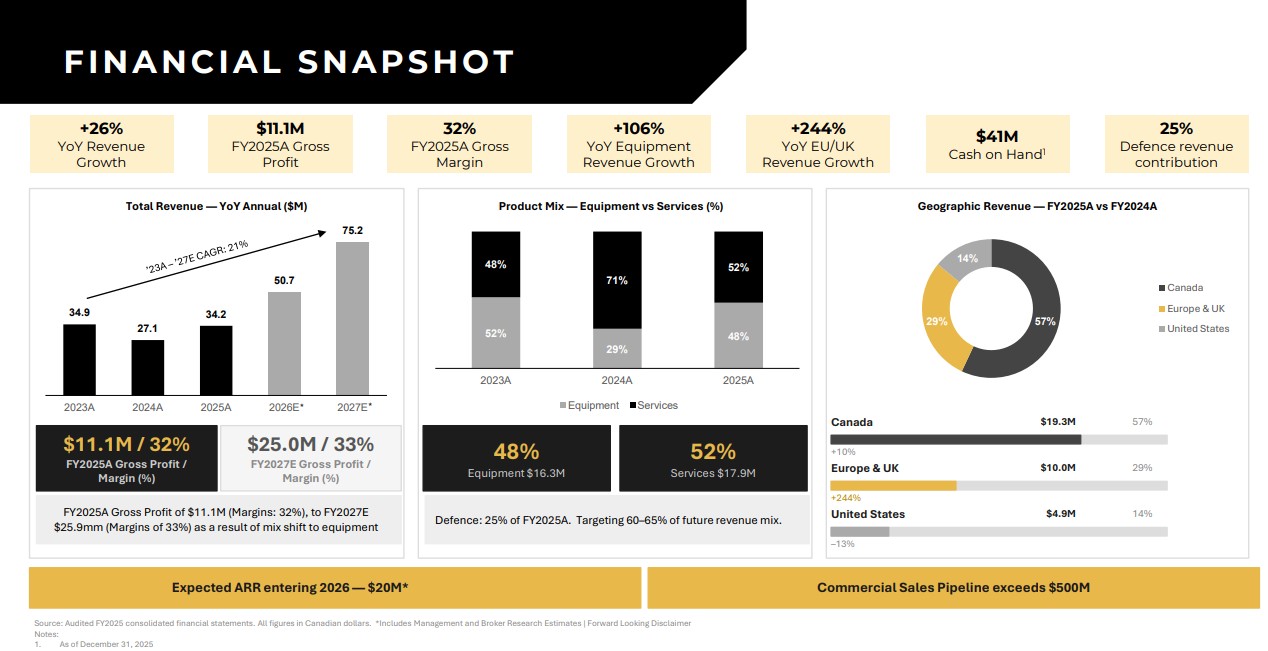

Recent capital raising efforts underscore the phase of accelerated expansion. A significantly oversubscribed bought-deal financing of over CAD 30 million has strengthened the balance sheet and expanded the investment base for production expansion and technology development. The funds are primarily being directed toward manufacturing capacity, system integration, and the further development of autonomous platforms. At the same time, the company has a growing order pipeline in the defence and training segments, including NATO-related programs and government training initiatives. These projects strengthen the share of recurring revenue and increase the visibility of future sales. To date, the capital market has not adequately priced in this combination of financing security and government demand. Below is an overview of the most recently published figures for fiscal year 2025, including an outlook for 2026/27.

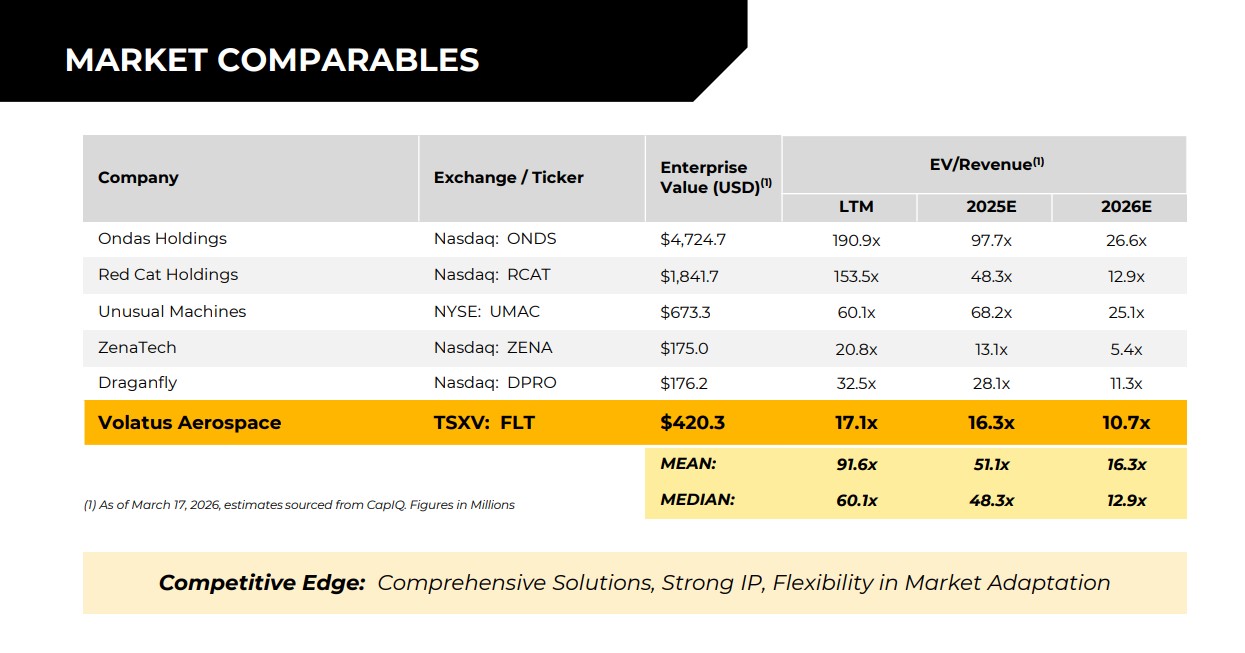

Valuation Discrepancy Between Growth Momentum and Market Capitalization

Despite rising operational activity, the valuation remains moderate in a peer comparison. Some competitors in the defence and drone segments trade at significantly higher revenue multiples, even though they exhibit similar or lower levels of diversification. Volatus, on the other hand, combines hardware, software, training, and services in an integrated model—an area competitors can only cover selectively.

The discrepancy between operational performance and market valuation opens up a potential re-rating scenario, provided that scaling in software and defence programs continues to gain momentum. The ability to systematically expand recurring revenue from SKYDRA and V-Cortex will be particularly crucial. In a market environment increasingly shaped by geopolitical demand and structural rearmament, this combination of platform depth and government demand could become a key valuation driver.

Investment Highlights

Volatus Aerospace (WKN: A2JEQU | ISIN: CA92865M1023 | Ticker Symbol: FLT)

- Highly specialized aerial data analysis as a unique selling point

- Development into a technical testing authority for critical infrastructure

- High security requirements of public clients ensure a constant deal flow

- International rearmament trends create strategic needs for defence solutions

- Necessary certifications and training requirements result in little competition

- Significant growth potential through internationalization in the medium term

- Scaling enables exponential growth for internationalization

- The use of V-Cortex AI and SKYDRA propels Volatus forward by leaps and bounds

- Integration into the North American defence ecosystem secures US and NATO contracts

- Highly liquid stock and still low market valuation of just CAD 435 million

Conclusion: Platform Logic as the Key to the Next Growth Phase

Volatus Aerospace is in a transition phase from an operational drone service provider to an integrated autonomy and defence technology platform. The combination of government demand, NATO integration, software monetization, and industrial scaling creates multiple parallel growth drivers. In particular, the combination of Canada-Ukraine technology transfer and US- and NATO-related programs elevates the strategic relevance to a new level.

Speed is of the essence now! Volatus Aerospace is on the verge of a potential revaluation: operational strength and capital market expectations should now align. Although the share has recently traded in the range of around EUR 0.43 or CAD 0.60, the analyst consensus on LSEG Refinitiv already indicates a significantly higher price target for the coming 12 months of approximately CAD 0.90 to 1.25. This points to an upward trajectory that clearly puts the current low valuation into perspective. However, what matters most is not so much the short-term price momentum, but rather the solid revenue pipeline that will translate into robust earnings in the coming quarters. Volatus could even exceed its own forecast in the coming years, as the order book continues to improve. The challenge remains to convert this high order volume into operating profits, as the medium-term outlook offers significant upside potential!

CFO Abhinav Singhvi explained the company's strategy and its $500 million pipeline at the recent 19th International Investment Forum.

This update follows our initial report from March 2026. Click here for the initial report.